7 Ways to Increase Your Credit Score Quickly

Your credit score will determine whether you will get approval for credit cards, car loans, mortgages or other loans, as well as affect the interest rate you will pay. If you are not satisfied with your credit score today, do not worry: there are some simple ways to improve it quickly. Once your credit score improves, you can enjoy benefits like lower interest rates and insurance.

Keep in mind that while these tips will help you increase your credit score quickly, be patient and remember that it may still take 30-60 days to see any noticeable improvement.

Ratio of credit utilization.

Your credit utilization ratio represents 30% of your credit score. It is the number that shows how much debt you have compared to your total available credit. The more unused credit you have available, the lower your ratio.

For example, if the credit limit on all your cards is $ 10,000, but you owe $ 8,000, your credit utilization rate is 80%. You're using 80% of your credit.

That is quite high - a ratio of 30% or less is ideal. There are three main ways to reduce your rate of credit utilization.

1. Pay your Debt.

Using the above scenario, if you can pay your debt from $ 8,000 to $ 5,000, then your ratio is reduced to 50%. Once you lower your debt, your score will see a significant momentum quickly.

2. Request an Increase in Credit Limit.

If you are not able to come up with some money to pay off your debt quickly, try to get your credit card issuer to raise your limit.

If instead of having $ 10,000 in available credit, you have $ 15,000, your ratio would drop to 53% with a debt of $ 8,000.

Keep in mind, however, that you will usually only grant this if you have had a good record with them during the past year. If you have not received payments, you may not be able to get the raise.

Credit history.

The length of your credit history represents 15% of your score. If your score is low because you are new to credit then you will just have to be patient. But you can accumulate your credit by opening accounts now and keeping them in good condition in the future.

raise your credit score4. Keep the cards open.

You should not close any existing accounts, as each continues to contribute to your credit history. In fact, many people have the mistaken belief that closing credit card accounts will help their credit score when it is likely to have the opposite effect. The longer you have your accounts, the more you add your score. Even if you no longer use your old credit cards, you can cut or block the cards, but do not delete them.

5. Become an Authorized User.

If you have trouble getting approved for new accounts, see if you can become an authorized user on someone else's card. But be sure to sign up with someone who is a responsible user. Your score can drop dramatically if that person loses payments or has too much debt on that card, too.

Types of Credit.

The types of credit in use also represents 10% of your credit score. These formulas favor those who have various types of loans, including mortgage loans, auto loans, student loans, credit cards and store credit cards.

6. Mix your forms of credit.

While you should not borrow money for a house or car just to try to improve your score, it is worth bearing in mind that even opening a store credit card and using it for some small purchases can help improve your credit score slightly.

You may also consider opening a specialized card as a branded gas card (which only works for gas station payments). This will help you resist the urge to spend on other things and you accumulate rewards in no time like free gas.

Pay the balance immediately after each use and your credit score will reflect your good credit history, payment history and credit increase available.

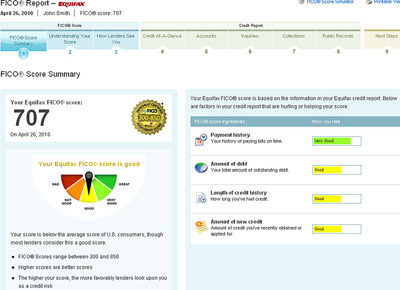

Payment history.

Your payment history is the highest percentage of your score - 35%. You should not avoid the importance of paying your bills on time.

7. Configure alerts and automatic payment.

Sometimes the payments are lost simply because the invoice was forgotten or lost. These little mistakes add up to your credit score. If you have trouble remembering to pay your bills, set up automatic payments or create reminder reminders on your calendar. There are no excuses!

Credit Tracking.

To maintain a good score, you must be diligent about supervising your credit, too. Check your credit report every year at AnnualCreditReport.com or MyFico to make sure there are no errors. If you notice a discrepancy, act quickly.

Your credit score may be unjustifiably low and you may simply have to make a call to correct any problems. In fact, studies have shown that up to 80% of consumer credit reports have an error, which may be costing up to 50 credit points.